Oclaro’s quarterly revenue up 28% year-on-year, despite 10G softness in China

source:Semi-conductor today

release:Nick

keywords: Semi-conductor Laser Technology Business news

Time:2017-08-12

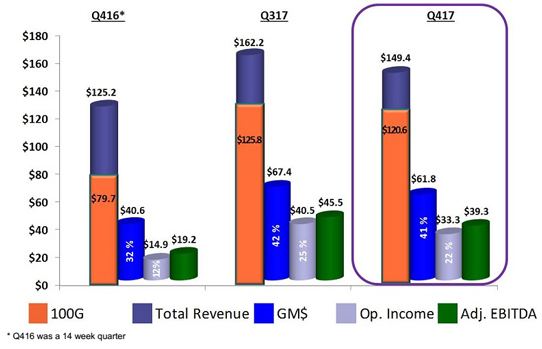

Despite quarterly revenue declining, non-GAAP gross margin fell only slightly, from 41.6% last quarter to 41.4%. This is up on 32.4% a year ago, driven by a richer 100G product mix and great scale as Oclaro further leveraged its manufacturing overhead. Full-year gross margin has grown from 29% in fiscal 2016 to 39.5% in fiscal 2017.

Operating expenses have risen further, from $25.7m a year ago and $27m last quarter to $28.6m (19% of sales), due mainly to R&D expenses.

Operating income was $33.3m (22% of revenue), down from $40.5m (25% of revenue) last quarter but more than doubling from $14.9m (12% of revenue) a year ago. Full-year operating income has risen from just $25.1m in fiscal 2016 to $130.9m (20% of revenue) in fiscal 2017.

Net income was $33.9m ($0.20 per diluted share), down from $39.9m ($0.23 per diluted share) last quarter but more than doubling from $14.4m ($0.11 per diluted share) a year ago. Full-year net income was $130.1m ($0.79 per diluted share) for fiscal 2017, up from just $19.2m ($0.17 per diluted share) in fiscal 2016.

Adjusted EBITDA was $39.3m, down on $45.5m last quarter but more than doubling from $19.2m a year ago (boosting full-year adjusted EBITDA from $40.9m in fiscal 2016 to $151.6m in fiscal 2017).

Hence, after subtracting capital expenditure (CapEx) of $18.4m (cut from $21.7m last quarter) and working capital (mostly related to inventory) of $15m, overall cash, cash equivalents, restricted cash and short-term investments rose during the fourth quarter by just $2.7m, from $254.8m to $257.5m.

For fiscal first-quarter 2018 (to end-September 2017), Oclaro expects revenue to grow to $151-159m, despite China revenue expected to be down by about 15% sequentially (then flat to down in fiscal Q2 - “We expect revenue from our 40G-and-below product to be relatively flat in the range of high 20s to $30m per quarter throughout fiscal year 2018,” says Dougherty). Gross margin should fall slightly to 38-41%, due to the proportion of new products in the mix, plus bringing on extra depreciation of about $1m per quarter. Operating income is expected to be $30-34m (falling to 20-21% of sales).

“As we enter fiscal year 2018, we expect to see continued high demand for our 100G-and-beyond products [specifically QSFP28 and ACO] in the data-center and metro markets,” says Dougherty. “We will be able to maintain our gross margins in the high 30s below 40 percentage range. This margin translates into operating income in the high-teens to 20% range,” he adds. “We also expect to continue to generate cash throughout the year.”

Going forward, operating expenses are expect to be steady at 19-20% of sales. CapEx for full-year fiscal 2018 should be $65-75m (similar to fiscal 2017). “For the year we expect spending to be front-end loaded and to add about $1m per quarter in depreciation,” says chief financial officer Pete Mangan.

Despite two strong headwinds (the market in China – which is expect to be flat to down in the December quarter – and the ramp-down of the client-side CFP platform as the market transitions to the QSFP28 form factor), for calendar full-year 2017 Oclaro still expects revenue growth of about 20% on 2016. This implies that second-half calendar 2017 will be relatively flat on the first half (with growth for QSFP28 and CFP2-ACO again compensating for China being flat to down).

“While we continue to expect the healthy market in the Americas and a slower China market for us over the next couple of quarters, we still believe the fundamental demand drivers in China remain intact,” comments Dougherty. “We anticipate growth from the region to return again later this fiscal year, driven by new metro and prudential network deployment.”

Growth in China should be further aided by an increase in demand for 25G and 100G optical transceivers used in 5G front-haul deployment. “We are well position to serve what could be a very significant new market for Oclaro due to these transceivers requiring industrial operating temperature ranging. Our laser chip and packaging technologies enable us to address this requirement and differentiate ourselves in this market,” says Dougherty. “While we will likely see most of the growth over the next few quarters from the ACO and QSFP28 product family as both the metro and data-center market upgrades to 100G and beyond, we expect both of these markets to stay strong throughout fiscal year 2018, particularly in North America and gradually building in China,” he adds.

Oclaro has appointed Ian Small to serve on its board of directors (effective 1 September). Most recently chief data officer of Telefónica S.A., Small has competencies in communications services, digital services, technology innovation and strategy. On 27 July, Oclaro increased the size of the board from seven to eight, and Small will serve as a Class II director.

4th Collaboration! What Brought the Global Laser Academic Guru to Chinese Univs & Leading Firms?

4th Collaboration! What Brought the Global Laser Academic Guru to Chinese Univs & Leading Firms? DNE Laser Foshan Smart Manufacturing Base Grand Opening: New Brand Image Starts New Journey

DNE Laser Foshan Smart Manufacturing Base Grand Opening: New Brand Image Starts New Journey Live: DMP GBA Expo – Laser Hard Tech Leads Industrial Smart Manufacturing New Wave

Live: DMP GBA Expo – Laser Hard Tech Leads Industrial Smart Manufacturing New Wave Scientists Develop Palm-sized Short-pulse Laser System: Efficiency Increased to 80%

Scientists Develop Palm-sized Short-pulse Laser System: Efficiency Increased to 80% Global LiDAR Giants Engage in Escalating Patent Wars

Global LiDAR Giants Engage in Escalating Patent Wars Shi Lei (Hipa Tech): Focus on Domestic Substitution, Future Layout in High-End Laser Micromachining

Shi Lei (Hipa Tech): Focus on Domestic Substitution, Future Layout in High-End Laser Micromachining Optizone Technology: 17 Years Devoted to Optics – High-Power Optics Mass-Production Pioneer

Optizone Technology: 17 Years Devoted to Optics – High-Power Optics Mass-Production Pioneer Zhuojie Laser: Breaking barriers via tech breakthroughs, aiming to lead high-end light sources

Zhuojie Laser: Breaking barriers via tech breakthroughs, aiming to lead high-end light sources Dr. Sun Linchao: Pioneer and Leader in China's Field of Medical Aesthetic Laser Therapy

Dr. Sun Linchao: Pioneer and Leader in China's Field of Medical Aesthetic Laser Therapy Guo Guangcan, CAS Academician & USTC Professor: Four Decades Chasing Quantum "Light"

Guo Guangcan, CAS Academician & USTC Professor: Four Decades Chasing Quantum "Light"